Last updated: 29 / 06 / 2026

The VSME standard (Voluntary Sustainability Reporting Standard for non-listed SMes) is a voluntary sustainability reporting standard specifically designed for small and medium-sized enterprises (SMEs). Developed by EFRAG, it provides SMEs with a tool that can easily supply the sustainability data requested by banks, investors, or large clients, within a framework of sustainable economics.

Do you want to implement VSME? ETERNITY Systems explains everything about this voluntary standard, its application challenges, its benefits and its implementation.

- The VSME standard in summary

- What is the VSME standard?

- What are the objectives of the VSME standard?

- ESRS, CSRD and VSME: what are the differences?

- How is the VSME standard structured?

- Which companies are affected by the VSME standard?

- What are the advantages of VSME?

- What are the key steps in implementing VSME?

The VSME standard in summary

- La VSME standardDeveloped by EFRAG, it allows small and medium-sized unlisted companies to structure their sustainability data (energy, CO₂, working conditions, governance) in a streamlined format proportionate to their resources.

- VSME offers two modules : a basic (Core) with a minimal set of simple indicators, and a complete (Comprehensive) for more advanced companies, which wish to strengthen their transparency with additional indicators.

- By adopting the VSME, SMEs strengthen their credibility with banks, investors and major clients, thanks to clear, reliable and harmonized indicators.

What is the VSME standard?

The VSME standard gives to small and medium-sized enterprises (SMEs) not listed on the stock exchange a simple regulatory framework to account for their sustainable practices. It was developed by EFRAG (European Financial Reporting Advisory Group) at the request of the European Commission, within the framework of the package of measures to support SMEs of 2023.

The VSME standard complements the CSRD directive., which is aimed at companies with more than 1000 employees. It adapts the requirements of sustainable reporting to the realities of SMEs, with a voluntary, simplified framework proportionate to their resources.

In practice, before investing, banks, investors, and major clients expect companies to demonstrate that they meet certain environmental and social criteria. It is with this in mind that the VSME standard was designed, to enable SMEs to have of a tool that allows them to transmit this ESG (Environmental, Social and Governance) information and strengthen their credibility, while avoiding an excessive administrative burden.

What are the objectives of the VSME standard?

The VSME standard pursues three main objectives:

- To provide a framework adapted to micro-enterprises and SMEs to monitor their performance and better manage sustainability with simple indicators proportionate to their size.

- Reducing ESG reporting costs: Many SMEs receive various requests from their customers, such as energy questionnaires, forms on working conditions, or CO₂ emissions surveys. The VSME harmonizes these expectations by providing a reporting framework recognized by all.

- Facilitating access to financing and public procurement: By adopting the VSME (Value-Added System for SMEs), SMEs have access to credible and comparable data, aligned with European standards. This makes it easier for them to access green financing or public procurement.

These objectives are part of a context in which CSR is becoming essential. According to 2024 CSR barometer, 78% of companies now have a dedicated CSR team and 76% allocate a specific budget. This trend shows that sustainability in relation to the principles of reuse et circular economy has become a central issue for all organizations, including the smallest ones.

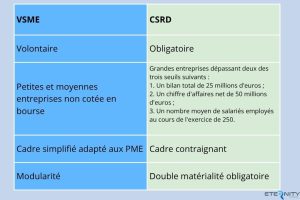

ESRS, CSRD and VSME: what are the differences?

Sustainability reporting in Europe Today, sustainability reporting is based on several texts and standards that address different categories of businesses. The CSRD mandates sustainability reporting for large companies, the ESRS specifies the rules to be followed for this reporting, and the VSME offers a voluntary and simplified alternative for small businesses.

- The CSRD (Corporate Sustainability Reporting Directive) : European directive which makes the publication of ESG information mandatory for large companies.

- ESRS (European Sustainability Reporting Standards) Technical standards published by EFRAG detail how to apply the CSRD. They define the indicators, ESG themes and the principle of dual materiality (analytical framework that examines the financial materiality and impact materiality of a company).

- VSME Standard : takes up the spirit of the ESRS in a simplified version for SMEs, adapted to their resources and needs.

What you must remember : The VSME opens the way to sustainable reporting for the smallest companies, in order to ensure an ecological and social transition accessible to all companies.

How is the VSME standard structured?

The VSME provides a clear framework with sustainability indicators divided into two modules:

- The basic module

- The complete module

The advantage of this modularity is that it simplifies and accelerates reporting, eliminating the requirement of dual materialityIndeed, with VSME, the company does not need to analyze both the impact of its activities on the environment and society, and the impact of these issues on its financial performance.

The basic module or “Core” module

The basic module establishes a minimum foundation of information on environmental and social issues. that all companies, even the smallest, can provide without excessive reporting complexity. This module includes 11 requirements and 49 indicators on the environment and governance such as:

- General information about the company.

- Sustainability commitments.

- Energy consumption and greenhouse gas emissions (Scopes 1 and 2).

- Water management.

- Working conditions and safety.

- Corruption prevention.

For example, in this basic module, a transport SME can indicate its annual fuel consumption and the measures put in place to reduce its emissions.

The complete module or “Comprehensive” module

The full module, or "Comprehensive", is aimed at companies that wish to strengthen their transparency and demonstrate a more advanced commitment to sustainability.

This module does not replace the basic module; it is added to it. A company therefore begins by publishing the information from the basic module, then supplements its reporting with the requirements of the full module when it reaches a certain level of maturity or when its economic context requires it.

The full module introduces 9 additional requirements and approximately 30 supplementary indicators as :

- Define a clear and consistent CSR strategy.

- Implement a climate transition plan aligned with international objectives.

- Calculate the company's full carbon footprint (Scopes 1, 2 and 3).

- Identify and assess the risks associated with climate change.

- Monitor and report human rights incidents in the supply chain.

- Declare income from sensitive or controversial activities.

Which companies are affected by the VSME standard?

The VSME standard applies only to micro, small and medium-sized enterprises with fewer than [number missing] employees that are not listed on the stock exchange. and which are not in the mandatory field of the Corporate Sustainability Reporting Directive (CSRD).

- Large companies reaching two of the following three thresholds: total assets of €25 million; net sales of €50 million; an average number of employees during the financial year of 250are covered by the CSRD and have been required to publish a mandatory sustainability report since 2025. The VSME does not apply to them.

- Listed SMEs They are also subject to the CSRD, unlike unlisted SMEs, and will also be required to publish a sustainability report, but according to a simplified schedule and format.

- The VSME also does not apply to these companies.

- Unlisted SMEs They are not covered by the CSRD. They can choose to voluntarily adopt the VSME.

- Micro-enterprises : they are included in the scope of the VSME if they wish to use it, without obligation.

The Omnibus package for February 2025 proposes to restrict the scope of the CSRD by raising the application thresholds (up to 1,000 employees and €450 million in turnover) and by postponing certain obligations, particularly for listed SMEs.

The aim is to simplify sustainability reporting and reduce the burden on businesses. These changes are still proposed and are not yet in effect.

What are the advantages of VSME?

Adopting the VSME standard and structuring sustainability reporting allows companies to:

- To have a competitive advantage,

- To better organize ourselves internally,

- To improve their access to financing,

- To anticipate regulatory changes.

A competitive advantage

The VSME is a recognized and common reference pointIn other words, it is easier to compare data because everyone uses the same benchmark and indicators. In practice, this allows companies using VSME to provide credible sustainability data on their environmental and social performance.

An SME equipped with VSME reporting is then better prepared to participate in tenders and meet the requirements of investors and business partners.

Better internal organization

VSME allows for the monitoring of specific indicators which track energy consumption, CO₂ emissions, working conditions, and social commitments. This provides clear benchmarks for managing operations and making decisions based on the results provided by these performance indicators.

For example, an industrial company can discover, through VSME, that its old equipment is responsible for the majority of its energy consumption and plan its replacement.

Better access to financing

The VSME facilitates access to loans and investments by providing reliable ESG data and presented in a standardized format. Banks and investors have all the necessary information to assess risks (e.g., energy dependence, human resource management or carbon footprint) and make their lending or investment decisions with confidence.

For example, a transport company that presents an energy transition plan within the VSME framework increases its chances of obtaining green funding to renew its fleet and reduce its emissions.

Anticipating regulatory changes

Companies that adopt VSME will not have to improvise an emergency compliance effort if the rules change. In other words, they are preparing now for future obligations that could broaden the scope of the CSRD.

What are the key steps in implementing VSME?

To implement sustainable reporting that tracks VSME indicators, there are several important steps:

- Assess the initial situation,

- Mobilize all teams,

- Organize the collection of useful data,

- Write the report,

- Taking action to improve.

Step 1: Assess the initial situation

The first step in implementing the VSME is to draw up an overview of current sustainable practicesA company needs to know where it stands in order to choose the module that suits its needs and objectives: the basic module, simpler and focused on essential indicators, or the complete module, more demanding.

For example, a building SME that already monitors its energy consumption may be satisfied with the basic module to start with, then move to the complete module when it develops a climate plan.

Step 2: Mobilize the teams

Sustainable reporting relies on the commitment of all teams within the company.If management is responsible for championing and supporting the project, then all employees must also be involved:

- First, teams need to be made aware of CSR issues by explaining why VSME is useful and how it works.

- Next, specific roles must be assigned to each person: CSR manager, accounting, human resources, etc.

For example, in an industrial SME, the HR team collects social data, maintenance provides data on energy and machinery, and management validates the CSR report.

Step 3: Collect useful data

The VSME relies on several concrete indicators such as energy, working conditions, governance, and CO2 emissions, which must be monitored and then analyzed:

- First of all identify where this information can be retrieved : electricity bill, accounting statements, HR register, etc.

- Then define a reference period on which the different indicators will be analyzed (monthly, quarterly, or even annual collection depending on the indicators).

- The ideal, finally, is to centralize all this data in a single tool easy to access and use.

For example, a transport SME can track the monthly fuel consumption of its vehicles to inform its annual CO₂ emissions.

Step 4: Write the sustainability report

Once the data has been collected and verified, the company must... present in a structured report which meets the requirements of the chosen module (Core or Comprehensive):

- The report must follow the order of the indicators defined in the standard : general information, environmental indicators (energy, CO₂, water, waste), social indicators (staff numbers, working conditions), governance indicators (ethics, anti-corruption, transparency).

- Simply publishing numerical data is not enough. because the company needs to interpret its results and explain why certain values are high, what progress has already been made, and what difficulties remain.

- The report must show a trajectory with measurable, credible objectives indicating the direction to follow.

- The language should be simple and accessible. with data presented clearly (tables, graphs, year-over-year comparisons). Transparency also means not hiding the difficulties encountered and those that exist.

- The report must be approved by management before publication..

Step 5: Publication of the report

For publication, the company must make the report accessibleeither on its website or by sharing it directly with its financial and commercial partners. Then, it is necessary to gather feedback from stakeholders and draw lessons from itThese feedbacks allow us to:

- To identify the shortcomings,

- To adjust data collection,

- To improve the accuracy of reporting from one year to the next.

The VSME standard illustrates a new way of approaching sustainable reporting for small and medium-sized enterprises.By offering a voluntary, simple framework aligned with European standards, it allows SMEs to structure their ESG data, improve their competitiveness and strengthen trust with their financial and commercial partners.

Following this same logic of supporting the transition, ETERNITY Systems develops solutions, such as the industrial washing, which facilitate the implementation of CSR initiatives adapted to the resources of SMEs. The objective: to give every company the means to make a concrete commitment to sustainable and responsible development, regardless of its size.

FAQ

What is a voluntary sustainability report?

A voluntary sustainability report is a document produced by the company to present its environmental, social and governance (ESG) practices. In the case of the VSME, it is a standardized framework that allows unlisted SMEs to structure this information and communicate it to their clients, banks or investors.

What are the penalties for non-compliance with the VSME?

Since VSME is a voluntary standard, no penalty is foreseen for non-compliance.It is based on the commitment of companies that wish to improve their transparency and meet the expectations of their partners.

What resources are available to facilitate the VSME standard?

The European Commission and EFRAG provide several support tools:

- Un multi-country project under the Technical Support Instrument 2025 entitled “Improving Sustainability Reporting for Businesses”.

- Le EFRAG SME forumdedicated to the exchange of best practices between companies.

- The application guides and digital tools to help SMEs complete their indicators more easily.

How often should sustainability information be updated?

Sustainability information must be updated at least once a yearThese financial statements, consistent with the closing of the accounting period, must be provided to shareholders 15 days before the Annual General Meeting, along with the management report. However, an update may be necessary during the year if a significant change occurs (new policy, major data development, significant incident).

About the Author

Communications and Marketing Manager at ETERNITY Systems, Anthony designs strategies and content to promote more sustainable consumption. He is a committed agent of change who combines creativity, rigor, and action to strengthen the visibility and impact of projects related to reuse and the circular economy.

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM

- Anthony ADAM